A Great Credit Score Isn’t Luck — These Strategies That Actually Work

Clear, Actionable Tips to Move From Poor Credit to Powerful Financial Leverage

This story is going to be all about building up a really good credit score, even if you’re working your way from the ground up.

Instead of giving you out-of-touch boomer financial advice, this series is all about the financial building blocks that actually matter to our lives in the 2026s.

And whether you’re still in college, starting your first full-time job, or simply just getting your money together for the first time, the most important thing is to make sure you have the right tools for where you are right now.

Okay, so first things first, what actually is credit, and why does it even matter in 2025?

Credit is essentially your financial reputation

Your credit score is the number that lenders use to judge your trustworthiness when you ask to borrow money.

Now, you may think that you want to just avoid borrowing money altogether. And as nice as that sounds, it’s not necessarily a very realistic ideal, especially in our current financial landscape.

If you ever want to buy a house, finance a car, take out a business loan, refinance your student loans, or do any other number of things, you’re probably going to have to apply for credit.

Even getting approved to rent an apartment often requires proving a good credit score, especially in big cities like New York.

Some employers may even check your credit score before they decide whether or not they want to hire you.

A good credit score can mean lower interest rates, better mortgage terms, better loan terms, higher limits on your credit card, better access to credit cards with very good reward systems, easier apartment approvals, and the list goes on.

On the other hand, bad or no credit can cost you thousands of dollars in the long run based solely on paying higher interest rates, and it can make it harder to get things like an apartment or your utilities in your name.

Now, a bad credit score is not a reflection of your value as a person, and it’s not even a judgment call on your level of responsibility.

You can even be good with money and have zero credit history. It’s a purely pragmatic number that you need to build up; it could just be a real hindrance to navigating adulthood.

To illustrate the importance of having a good credit score, let’s look at how score ranges affect car loan rates.

According to Experian, on average, a new car buyer with an excellent credit score can secure an average interest rate of 5.18%. But that average jumps to 15.81% for borrowers with poor credit scores. For used car buyers, those averages range from 6.82% to 21.58%, depending on the borrower’s credit history.

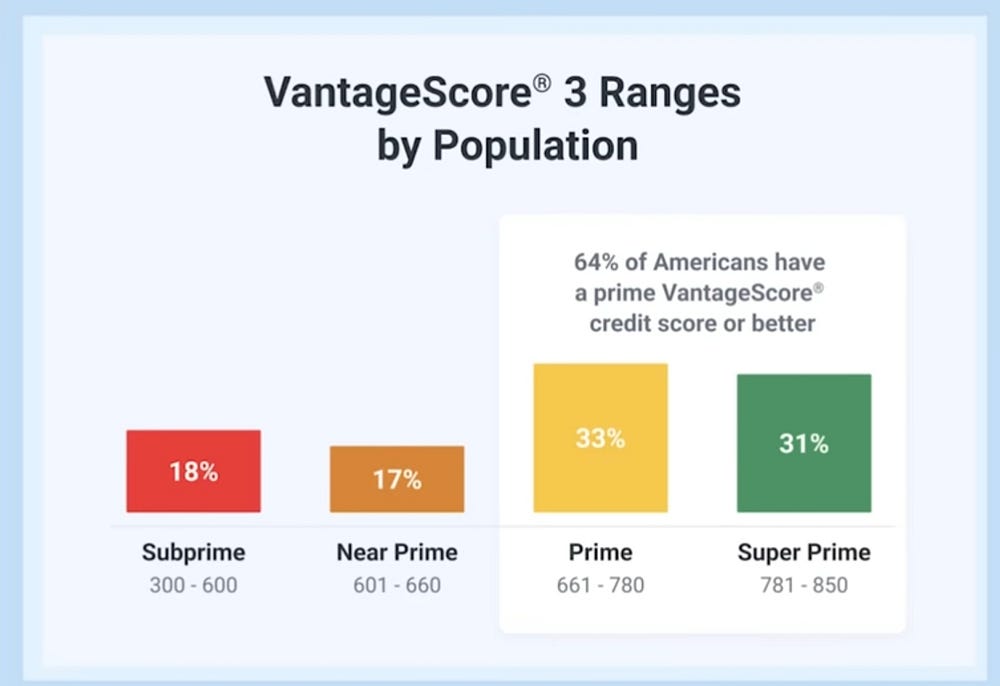

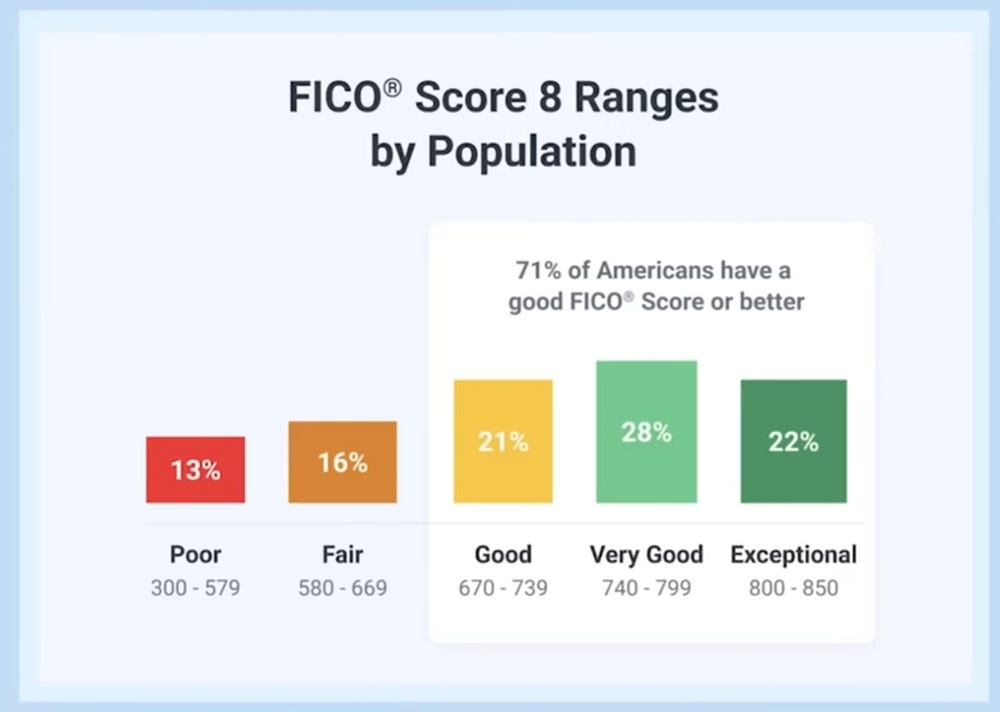

What qualifies as a good versus a bad credit score?

There are three main credit reporting bureaus: Equifax, Experian, and TransUnion, and two main credit scoring models: FICO and VantageScore.

Generally, for both, a score in the mid-600s to mid-700s is good. Anything above that is very good, excellent, or exceptional.

Here are some visuals breaking down each scoring model’s ranges. And the way that these two scoring models calculate their scores is a little bit different.

VantageScore was created in 2006 by the three main credit bureaus. Its scores are used by a variety of financial and non-financial institutions for lending products such as credit cards, auto loans, mortgages, and tenant screenings.

Additionally, VantageScore uses data like your rent and utility bill payments to create your credit profile and can calculate your score after your credit account has been open for at least one month.

FICO scores, on the other hand, have been around for over 25 years now and are typically used much more often by lenders.

These are the factors that make up your FICO score. Payment history makes up 35% of your score.

Paying on time is the absolute biggest factor. Even one missed payment can drop your score significantly.

Credit utilization makes up 30%. This is how much of your available revolving credit you’re using.

For instance, if you have $10,000 of available credit across lines of credit and credit cards, and your outstanding balances add up to $3,000, your current credit utilization rate is 30%.

- Length of credit history makes up 15%. This is the average age of your accounts, and older is better. This is the trickiest factor to overcome when you don’t have credit to begin with, which does mean that the earlier you apply for your first loan or credit card, the better.

- New credit inquiries make up 10%. This means that opening too many accounts at once can actually ding your score temporarily.

- Credit mix makes up 10%. Lenders like to see that you can handle different types of credit, like credit cards, student loans, car loans, etc.

Credit really is a balancing act. And at the end of the day, what’s going to boost your score on one system is likely also going to boost your score on the other scoring model.

So now that you know the basic building blocks of building your credit score, let’s look at some more insider tips for building credit, especially when you have no credit history to speak of.

#1. Lower your credit utilization rate

So this is probably a lesser-known way to boost your credit score, but it is one that a lot of experts recommend, and that is keeping your credit utilization rate under 10%.

The typical advice to keep up a good credit score is to keep your utilization rate lower than 30%.

But even lower, to 10%, is A+. Now, this does not mean keeping it at zero. Lenders want to see that you can continuously and responsibly use and pay back credit.

So, in order to lower your utilization rate, definitely focus on paying down current debts, especially high-interest debt.

And you could also ask your current lenders to increase your credit limit, and then just not increase your spending at all on your card after that.

And of course, it is super important to pay all of your credit card bills in full and on time, both for maintaining a stellar repayment history for your credit score and keeping that utilization rate low, but also just not getting yourself stuck in a cycle of debt.

#2. Apply for a secured credit card

Now, this is a great option for people without an established credit history because you don’t typically undergo a credit check in order to obtain a secured credit card.

These kinds of cards require you to put down a deposit that acts as collateral.

Your deposit then becomes your credit limit, and you use it like a normal credit card.

You still pay off your balance every month, but if you miss any of your payments or default on your card, your lender can fall back on that deposit you made, hence how it works as collateral.

#3. To become an authorized user

This works if you have a parent or family member who has a credit card they can add you to.

And this gives you a credit card in your name that is attached to their account.

Now, they have to trust you not to mess up their credit because while this helps boost your credit score, they are still liable for any bills you don’t pay.

But luckily, you don’t actually have to use the card all that much for it to make an impact.

Just being added as an authorized user at all can help establish your credit history and be a real boon to your score.

And lastly, consider utilizing a rent reporting service. There are services out there that will report things like your rent and utility payments to credit bureaus.

This means you can take advantage of payments you’re already making to help establish and build your credit.

The one potential downside is that these types of services usually do cost money.

Now, credit scores have long been pretty consistent in how they’ve worked for a couple of decades now.

But we can’t end this story without talking about the new bombshell who has entered the villa, and that is buy now, pay later apps.

Until now, buy now, pay later app usage has existed outside the credit scoring system.

The apps can obviously be pretty attractive to people who don’t qualify for traditional credit cards.

However, FICO recently announced that it will begin incorporating BNPL history into its new scoring model. The new model, expected to launch this fall, was trained on a data set of more than 500,000 BNPL users in partnership with one of the main buy now, pay later apps.

According to The Wall Street Journal, FICO claims to treat BNPL accounts differently from credit cards, grouping multiple BNPL loans rather than penalizing consumers for opening several new lines of credit in a short period.

In early testing, FICO said it found that consumers with five or more Affirm loans typically saw their credit scores increase or remain steady under the new model, as long as payments were made on time.

And that’s the big caveat. If you use BNPL services and you do pay them off regularly, that could potentially boost your score.

But the opposite is also true. If you overdo it and you miss your payments, those apps are now reporting, and it could really hurt your score.

Buy now, pay later apps had already been reporting to debt collectors for overdue balances, which could have already been negatively impacting your credit score.

Essentially, we need to approach these apps the way we do any type of credit, only relying on them when we know we can make our payments in full and on time, not using them as an excuse to spend beyond our means, and avoiding them altogether if they make overspending just too easy.

Again, building up a really good credit score is not a prerequisite for being a good or interesting or valuable person, but it is a really important tool for getting your life together and building up the life you want, financial and otherwise.

Thanks For Reading 🙂