Your Savings Could Be Growing Faster — Best High-Yield Accounts for 2026

Discover which banks are offering the highest APYs, best features, and strongest savings benefits this year

High-yield savings accounts are one of the easiest ways to have your cash earn more interest.

But it’s reported that only20% of Americans leverage these accounts, where another study by CNBC shows significantly more people use traditional savings over high-yielding ones.

#1. What are high-yield savings accounts?

To simply put it, high-yield savings accounts are a type of savings account that allows you to earn more interest on your cash that’s sitting.

For example, Traditional Bank Accounts

- Chase pays you a 0.01% of interest on your cash sitting.

- Where many high-yield savings accounts right now allow you to earn around 3 to 4% of interest.

- The difference would actually allow your money to keep up with inflation.

- With a traditional one like Chase, you are pretty much losing value on your money every day.

This also realizes that one of the biggest reasons why high-yield savings accounts have become more popular is that many are coming from online-only banks that don’t have the cost of running physical branch locations, so they can offer much higher rates to attract their customers into their ecosystem.

But aside from that, with high-yield savings accounts, at least the right ones that I’m about to mention in this story, they are still FDIC insured up to $250,000.

And also know that high-yield savings accounts are not considered an investment, so there is no downside risk to losing money.

They’re also super liquid, which means you can easily gain access to your cash whenever you need it.

And many accounts, which I’ll show you some of the top ones later in the story, typically have:

- No fees.

- No balance requirements.

#2. Why did I start using them?

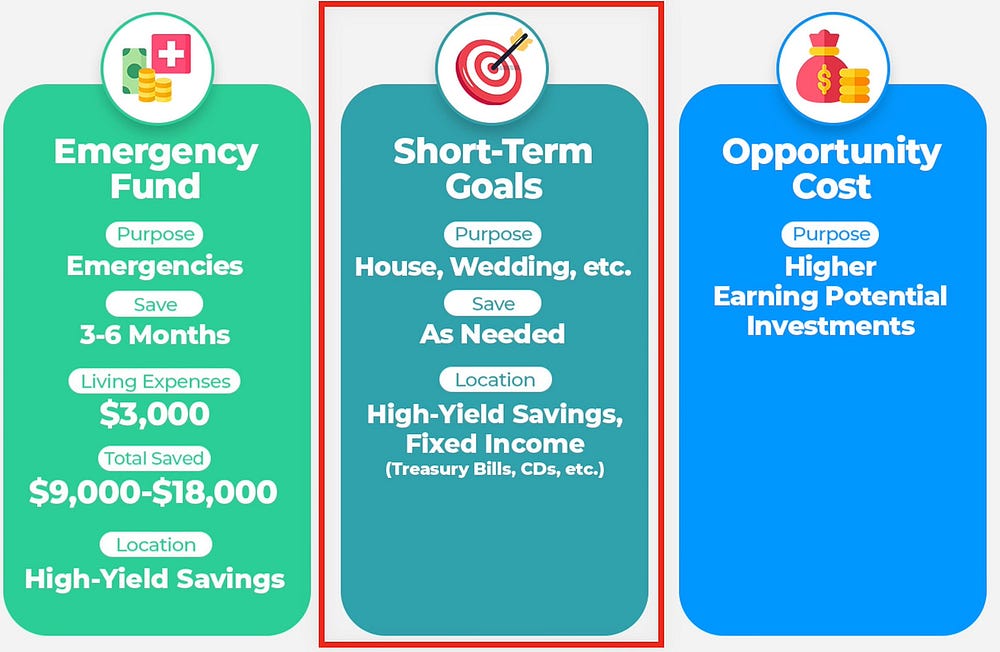

So, the first reason that is extremely important to understand and is a general guideline in the financial industry is to have an emergency fund in place for the worst-case scenario of something like a medical bill or car repair that could happen at any instant.

So, the amount to save for this is generally recommended to be about 3 to 6 months of your living expenses.

So, if you have $3,000 in living expenses, you would ideally want to aim for 9 to 18,000$ saved up.

Now, this may very well take you some time to build up, but if you stay consistent with it, you may be in a much safer position before you even know it.

So, let’s say that you do this and you put $10,000 into a high-yield savings account where you can earn a 4% APY, which stands for an annual percentage yield.

And if we assume that that amount stays the same throughout the entire year, all that means is that you would end up earning $400 in interest from the account.

But if you were to use a traditional bank account like Chase. That pays a 0.01% of interest, which means that after a full year, you would earn $1.

The thing here is that these traditional savings accounts from big banks like Chase or Bank of America are pretty much using your money to go and make them more money.

So, by using a high-yield savings account for your cash, you are now able to make more on your own rather than the big banks making money off of you.

But aside from using it as an emergency fund, high-yield savings accounts can be used for other short-term savings goals where you need the cash to be liquid, you want it to earn some money, but you don’t necessarily want to lock it away into CDs.

Or other types of bonds. So, whether that be saving for a down payment on a house, an upcoming wedding, or a large vacation trip you want to do, which if you need to straighten up your finances, many of these accounts also allow you to easily set up automatic transactions, so that if you want to build up an emergency fund, you could pretty much treat it as a bill that you have to pay.

It is super easy to set up and can really help you get into a better position before you even know it.

#3. Key Things To Be Aware Of

Now, the first point to mention here is that the interest you earn from high-yield savings accounts is going to be taxed as ordinary income.

So, let’s say that you earn $400 throughout the year with a new high-yield savings account.

If you’re in the 22% federal tax bracket, that would be $88 that you’d have to pay in taxes, leaving you with $312 in earnings, which doesn’t include any state tax if that applies to you.

But it’s still much better than using traditional savings accounts, and you’re at least getting in a few hundred dollars more than if you didn’t.

Aside from that, also realize that the interest rates you can earn through high-yield savings accounts can change at any instant.

The reason is that these rates are influenced by the Federal Reserve’s decisions on interest rates, which means that they are very likely to change over time.

But do know that even if the rates drop, high-yield savings accounts are still great for short-term savings goals to remain safe, liquid, and they’d still earn you much more interest sitting there than in a traditional savings account like Chase or Bank of America.

In the end, just realize that the rates you see today are not guaranteed long-term like they would be if you were to get a fixed income security like CDs or Treasury bills.

Which I will say, if you want to compare some of the top CD rates that you can currently get.

#4. How To Earn a Higher Interest

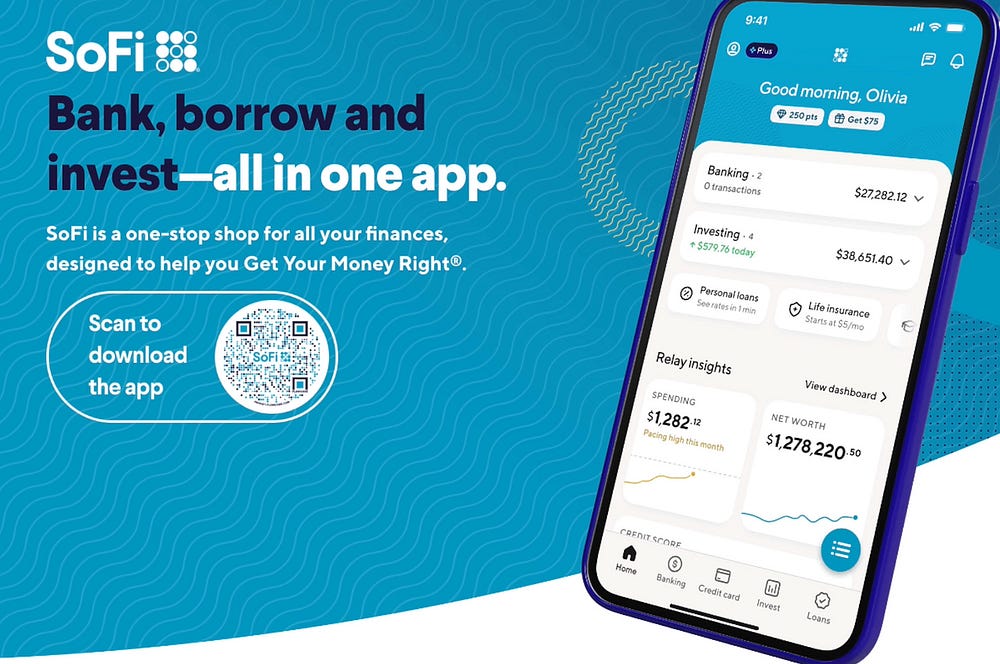

The account that I primarily use and recommend to nearly anyone is from the company SoFi,

- You may have heard of their SoFi Stadium.

- NBA commercials.

- The fact that they have 12.6 million members, or even that they are ranked number 27 in finance on the App Store.

But do know that their high-yield savings account currently offers a standard rate that is 3.3% of interest, and if you’re new, you can get a 6-month boost to that yield to make that 4% and even up to a $300 cash bonus.

They also offer zero account fees, and they are FDIC insured, which can also be up to 3 million dollars through their program.

And above all that, I personally think that they have one of the easiest platforms in the industry to manage your finances on the go.

Which also knows that this SoFi account is both a checking and a savings account, where they will provide you a debit card, but you don’t have to use it.

- There are no fees.

- You can even freeze the card if you’d like.

- But the biggest downside of all that can turn some away from SoFi is that to earn the higher interest and even the bonuses that they offer.

- You need to either set up an eligible direct deposit, transfer $5,000 worth of qualified deposits every 31 calendar days, or pay the SoFi plan subscription fee, which is $10 every 30 days.

But to summarize the meaning of the direct deposit, understand that this means a recurring deposit of regular income.

To an account holder’s SoFi checking or savings account that includes payroll, pension, or government benefit payments made by the account holder’s employer, payroll, or benefits provider, or government agency.

Now, if you do not want to change your main paycheck to go to SoFi, understand that you can easily do this with other potential income sources you have, where a few common ones include:

- DoorDash

- Uber

- Instacart

- Patreon

- Upwork

- Rover

- care.com

- Etsy

- Google Ads.

#5. Best For APY

Now, of the highest-earning accounts in the market, the first to mention here is Bread Savings, where you can currently get a 4.05% APY with their high-yield savings account, where they are FDIC insured, and all you need is a $100 minimum deposit.

But the offset here compared to one like SoFi is that they offer fewer features, but if all you care about is the APY, then this would be a top option to consider.

After that is also Western Alliance Bank, where you can see they’re currently offering a 3.9% APY.

They are FDIC-insured, and they require $500 to get started. And do know that there are no account fees.

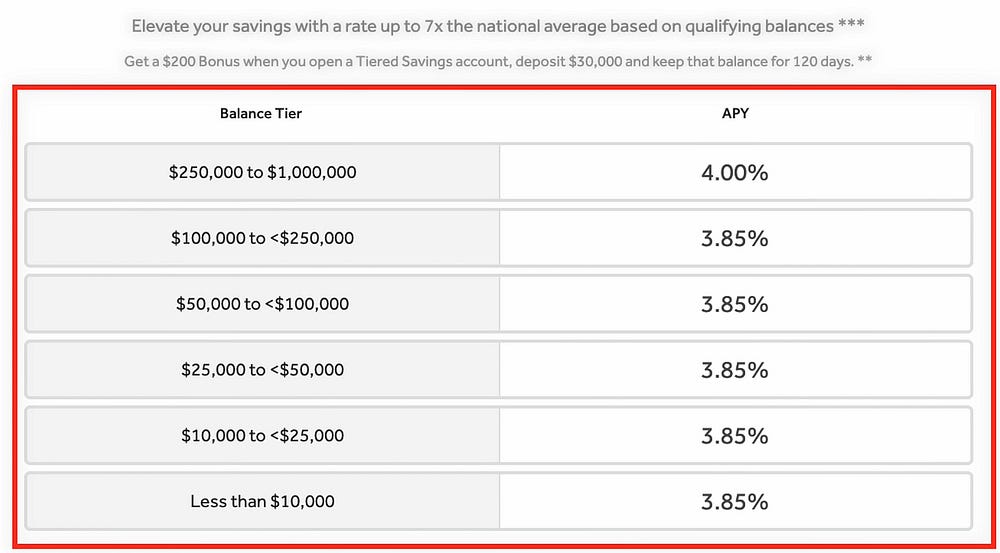

Besides that, we then have Barclays, which is offering up to a 4% APY and even a $200 bonus if you deposit over $30,000 within the first 30 days of opening the account.

But if that doesn’t apply to you, notice that the rates you can earn are based on the amounts you have.

So, the standard rate for most is 3.85% currently, and that this account currently has

- No monthly maintenance fees.

- No minimum balance requirements to open the account and get started.

On top of that, another option to think about is Valley Direct, where they are currently offering a 0.6% APY for 12 months, where you can currently earn a 4% yield if you are a new user.

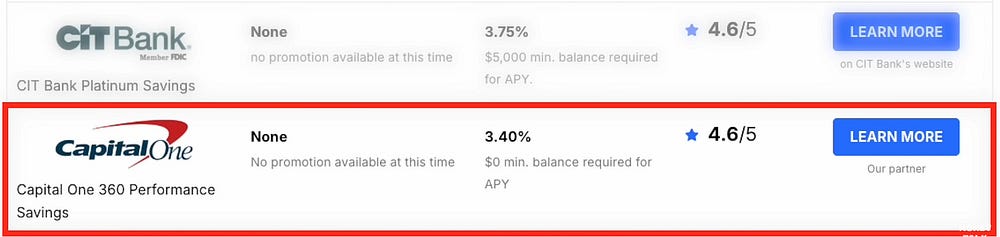

And then, the last one I’ll mention that is typically on the upper end, as well as far as competitive rates, is through CIT Bank, where they are currently offering a 3.75% APY.

But do know that it is with their Platinum Savings Account, and with that, you would need at least $5,000 in the account to earn the higher rate; otherwise, you’ll only earn 0.25% APY.

#6. Best For Credibility

For some, having a known bank may feel more trustworthy to have your money sit there, but you may also see that it is more convenient if you already have a bank account with one of the ones I’m about to mention.

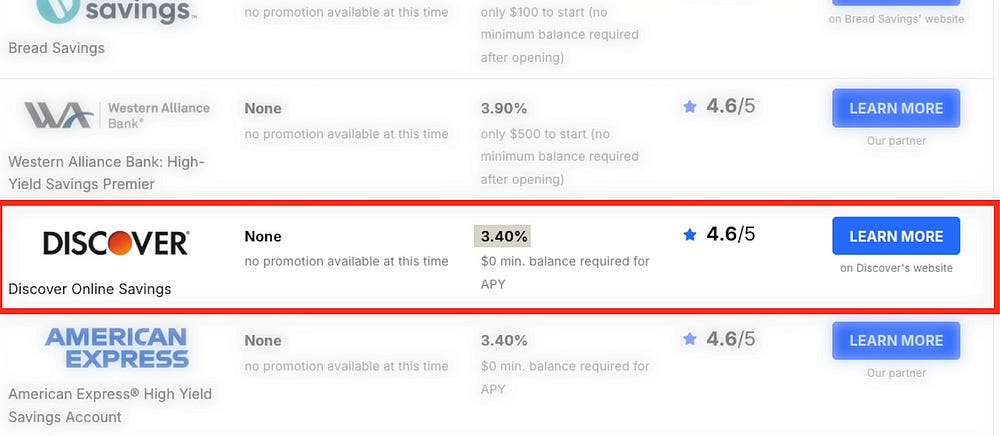

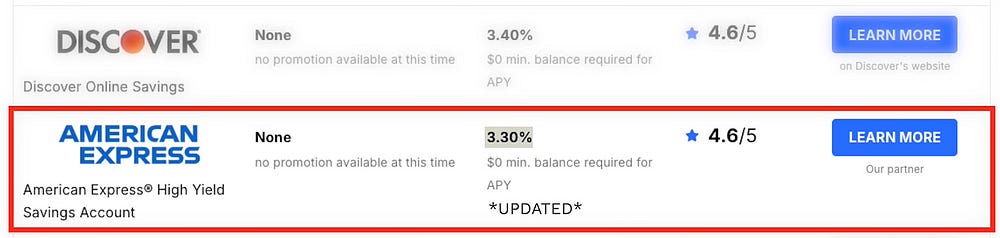

1. Discover

Now, Discover is currently paying out a 3.4% APY on its high-yield savings account, where they have

- No monthly fees

- No minimum opening deposit

- No balance requirements

- Real customer service from real people

- They are FDIC insured

2. Capital One.

As far as Capital One, they have their 360 Performance Savings Account that currently offers the same rate as Discover, with a 3.4% APY that includes:

- No fees

- No minimums

- They’re FDIC insured.

Now, Capital One also has a super clean and easy-to-use platform where they even have a few physical branch locations, where they’re mostly known for their Capital One Cafes.

3. American Express

They also offer a 3.4% APY and have many of the same features as Discover and Capital One.

All three are great options to consider and are much better than using traditional bank accounts like Chase or Bank of America.

#7. Best For Banking Features

1. SoFi

The current standard rate is 3.3% of a yield. And then, if you are new, you can get that 6-month boost to 4% and up to a $300 cash bonus.

But I mention SoFi again because they offer a super easy way to set up automatic features on their Autopilots page, which is the go-to place to view and manage your recurring deposits, withdrawals, and transfers.

Now, they also have a very convenient feature called Savings Vaults, where you can categorize your savings into different areas that you’d like, such as an emergency fund, house, taxes, wedding savings, you name it.

Not to mention, they also offer Zelle, many more modern features, and if you ever plan to use other products of theirs, like their SoFi Invest account.

2. Ally Bank

They currently offer a 3.3% yield. And although they do not offer any bonus offers on top of that, they have been known in the industry for their features, like their Savings Buckets that allow you to put your cash into different savings categories, just like the SoFi Vaults.

They also make recurring transfers easy to do, they offer a Round Ups tool, and even a Surprise Savings feature for those with a linked checking account, where they analyze your linked checking account and if they notice any spare money to move, they will transfer it to your savings.

So you don’t have to. Personally, I like to know what’s going on and have control of my own, but SoFi and Ally Bank are among the top two choices when it comes to simple features and overall options that they offer for your savings.

In the end, the choice really comes down to what you prefer most because you may want the highest APY possible, or you may want a temporary boost with any of them that you want to try out their certain ecosystem, or you may already have an account with a company that offers a high-yield savings account for a simple and easy integration.

Thanks For Reading:)